:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/GRXDZHK26NAAXPDXD6G6YNNG2M.jpg)

Nikhilesh De is CoinDesk's managing editor for global policy and regulation. He owns marginal amounts of bitcoin and ether.

Last Thursday morning, I wondered whether I needed to write a follow-up piece about Silvergate Bank. On Thursday evening, I wondered whether my main topic should instead be about ether potentially being a security. And then, obviously, some things happened.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

Registration woes

The narrative

Last week the New York Attorney General’s office sued KuCoin for operating an unregistered securities/commodities broker in the Empire State. Most of the complaint is pretty straightforward – the NYAG alleges KuCoin offered tokens that are securities under New York’s General Business Law (the Martin Act, which we’ve seen a few times before). More intriguingly, the suit alleged that ether (ETH), the second-largest cryptocurrency by market capitalization and one that has futures products built on top of it, was also a security listed by KuCoin.

Other details include the fact that KuCoin apparently did not bother responding to a subpoena from the NYAG.

Why it matters

If ether really is a security, that means every crypto exchange in the U.S. will need to register as a securities trading platform with the U.S. Securities and Exchange Commission (SEC) and abide by a strict disclosure regime that will probably make it difficult for many, if not all, of these exchanges to continue operating. But it’s a really big if.

Breaking it down

The NYAG sued KuCoin last week under state law, alleging that ether, post-Merge, is a security under the Ethereum blockchain’s proof-of-stake consensus mechanism. The NYAG also alleged that terraUSD (UST) and luna (LUNA) are securities, as well as KuCoin’s Earn platform. I’m not going to get into the last two – regulators have alleged for a while now that “earn” products are securities, and have settlements with various lenders to support that contention, and there are other cases looking at the terraUSD/luna ecosystem.

And not to pull a bait-and-switch on you but I have no answer to the question asked in the heading to this section. However, I did want to figure out what the result from the New York Attorney General’s suit against KuCoin could be.

Matthew Blaine, a New Jersey-based partner at the Davison, Eastman, Muñoz, Paone law firm, doesn’t think there will be much of a result.

The case is likely to end in adjudication, he said in a phone call.

“If there is any adjudication that [ether] is an unregistered security, it's not binding on any issue or things of that nature,” he said. “It really just has to be viewed in the narrow lens through which this case is proceeding.”

He compared the NYAG suit against KuCoin to the U.S. Securities and Exchange Commission’s (SEC) suit against former Coinbase director Ishaan Wahi. In that suit, the SEC alleged that a number of tokens were securities but did not sue Coinbase for listing the tokens, or the token issuers themselves.

Similarly, KuCoin hasn’t sued the Ethereum Foundation, just the one exchange, Blaine said.

It’s also unclear whether the NYAG is seeking registration from these other types of entities, or indeed from other crypto exchanges operating under the New York Department of Financial Services’ BitLicense.

The NYAG did not return multiple requests for comment, including a question as to whether it would require licensed crypto exchanges to register as securities trading platforms as well.

NYDFS is, of course, the state banking and financial services regulator overseeing all crypto companies, but the regulator’s authority may be challenged by the lawsuit.

One former NYDFS official told CoinDesk that the New York Attorney General’s office and the bank regulator did not have good relations while they were at NYDFS, describing those relations as a “perennial power struggle.”

The other factor is, of course, the SEC. SEC Chair Gary Gensler is on the record (a few times now) as saying he believes proof-of-stake cryptocurrencies resemble securities. The NYAG suit against KuCoin may not lead to much precedent for the SEC, but it’s still yet another sign regulators are starting to nail down what they’re thinking.

At least one judge, however, has very little patience with how the SEC is currently approaching these questions of whether or not something is a security. Judge Michael Wiles, of the New York Southern District Bankruptcy Court, wrote a pretty scathing order explaining his approval of Voyager Digital’s restructuring plan to sell itself to Binance.US, saying the regulator was not providing any clarity for industry operators.

“If the current regulatory environment can be characterized as uncertain, the future regulatory environment can only be characterized, in my mind, as virtually unknowable,” the judge wrote. “There have been differing proposals in Congress to adopt different types of regulatory regimes for cryptocurrency trading. Meanwhile, the SEC has filed some actions against particular firms with regard to particular cryptocurrencies, and those actions suggest that a wider regulatory assault may be forthcoming.”

Repeating his oral order from March 7, the judge went on to say the SEC’s arguments were vague and that the regulator did not provide any evidence backing up its arguments that Binance.US may be operating an unregistered securities exchange or that the VGX token might be a security.

“Although the SEC contended that the Debtors somehow had to prove a negative – i.e., that the Debtors were not violating securities laws and that Binance.US is not violating registration requirements for brokers – the SEC had not even affirmatively contended that the Debtors were doing anything wrong, or that Binance.US was doing anything wrong,” the judge wrote. “Nor had the SEC offered any guidance at all as to just what it was that the Debtors allegedly were supposed to prove on these issues, or how the Debtors possibly could prove what the SEC wanted them to prove without receiving any explanation at all from SEC as to just why the Debtors’ operations, or Binance.US’s operations, might raise legal issues.”

For further reading, I recommend my colleagues Sam Kessler and Cheyenne Ligon’s article asking what it means if ether really is deemed to be a security.

Stories you may have missed

- Santander, HSBC, Deutsche Bank, Others Still Willing to Serve Crypto Clients After Banking Failures, DCG Says: A Digital Currency Group memo obtained by CoinDesk’s Lavender Au says the venture capital firm is looking for new banks for its portfolio companies. (DCG is CoinDesk’s parent company.)

- U.S. Federal Reserve’s Real-Time Payments System Coming in July: FedNow is going to launch in July, giving U.S. financial institutions access to a real-time payment network.

- U.S. Treasury Department Proposes 30% Excise Tax on Crypto Mining Firms: The proposed 2024 budget suggested a 30% excise tax on crypto mining firms, among a number of other revenue-generating measures.

- Signature Bank, Stablecoins Might Benefit From Silvergate Exchange Network's Demise: Remember when there was really only one bank collapse in 2023? Those were the days. CoinDesk’s Helene Braun took a look at what the end of the Silvergate Exchange Network might mean for other companies.

The Great Banking Crisis

So the crypto industry just lost three banks that actually onboarded crypto companies: Silvergate, Silicon Valley and Signature. Their collapse has been seen by some as part of a coordinated conspiracy to de-bank crypto in the U.S., due to the timing and the explosiveness of the near-simultaneous failures.

In the aftermath, crypto companies are looking for alternatives (including CoinDesk, which banked at SVB). While this is going to be an interesting timeline in and of itself, another question may be what happens with the loss of the Silvergate Exchange Network and Signet, two tools created by Signature and Silvergate to allow crypto companies to process transactions 24/7.

Right now, Signet is still alive, but that may change if and when the FDIC sells Signature.

A Coinbase spokesperson said the exchange had contingencies in place should Signet be shut down.

"In that hypothetical situation, there are other players in the market that could step up to fill the void. As we saw over the weekend, crypto is resilient and we would absorb this and move on just as we have in other events,” the spokesperson said.

Dante Disparte, the chief strategy officer and head of global policy at stablecoin issuer Circle, said the two services helped build crypto, though he noted that ACH transactions and wire services also remain important.

“While [Signet and SEN] may go down in history as ignominious failures, they demonstrated that banks can innovate,” he said.

Another result may be that larger banks continue to gain new business while smaller community or regional banks and credit unions lose out, Disparte said.

One such company forced to make changes was Circle, whose USDC stablecoin lost its dollar peg for an entire weekend as a result of SVB’s collapse, starting on Friday and continuing after Circle acknowledged that it held $3.3 billion, or around 8%, of USDC reserves at the bank. The stablecoin finally regained its peg earlier this week.

There's also a matter of whether or not bank regulators are forcing banks to remove crypto clients. It’s a conspiracy theory that’s taken on fresh life in recent weeks, with everyone from lawmakers to industry participants saying “Operation Choke Point 2.0” is real.

Recent guidance from bank regulators, suggestions that Signature and Silvergate were forced to fold due to anti-crypto animus and news of the FDIC’s demands that Signature’s bidders not acquire its crypto business have bolstered these claims.

Disparte, however, does not believe it.

“I categorically reject the idea that this is Choke Point 2.0,” he said. “For one thing, [the original, Obama-era] Choke Point was covert, [but] this is overt … some companies create an unbankable asset.”

Other individuals CoinDesk has spoken to, including legal counsel at an exchange and a member of a Washington, D.C., lobbying group, also does not believe in Choke Point 2.0.

It may well be that banks are just derisking, and some crypto companies are genuinely riskier than others – Signature was reportedly under Department of Justice investigation prior to being shut down.

Austin Campbell, a Columbia University adjunct professor and former Paxos official, told CoinDesk that we may get an answer to this question over whether Choke Point is real within the next six months.

“The thing I would be watching is there's an obvious commercial voice for banks that can control risk. The crypto community should be watching to see if that's allowed, or if feds step in and block this,” he said. “If new banks step in and start servicing all these clients and onboarding them, then it's probably just a story of failures of risk.”

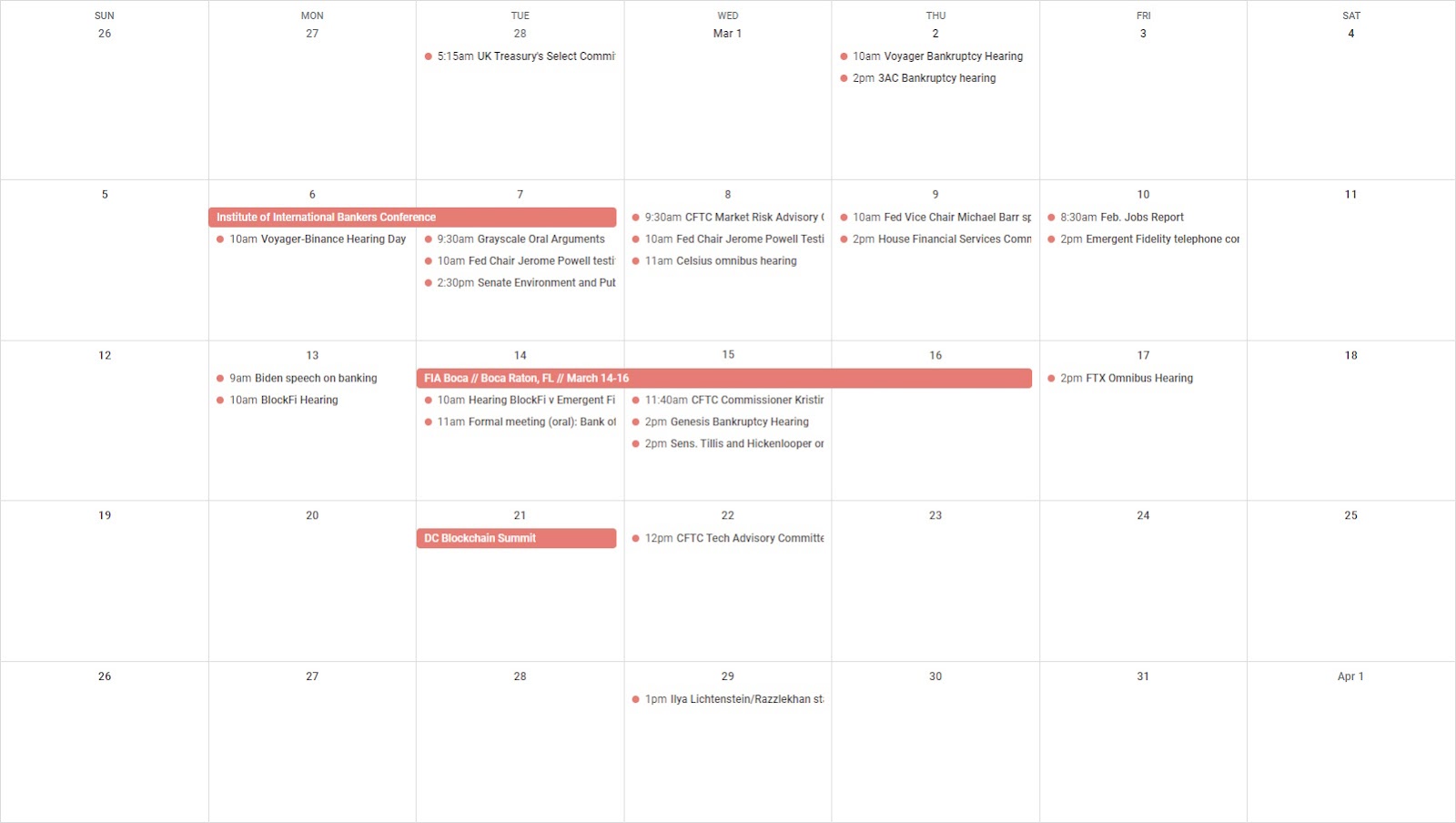

This week

Monday

- 13:00 UTC (9:00 a.m. ET) U.S. President Joe Biden addressed the banking events of the past few days.

- 14:00 UTC (10:00 a.m. ET) There was a BlockFi bankruptcy hearing.

Tuesday

- 14:00 UTC (10:00 a.m. ET) There was a hearing in BlockFi’s case against Emergent Fidelity over control of a number of Robinhood shares. Jack Schickler reports that BlockFi withdrew its motion without prejudice while the parties work on a potential compromise. A complicating factor may be the fact that the U.S. Department of Justice is also looking to seize the shares under a forfeiture motion.

Wednesday

- 18:00 UTC (2:00 p.m. ET) There was a Genesis bankruptcy hearing.

- 18:00 UTC (2:00 p.m. ET) U.S. Senators Thom Tillis (R-N.C.) and John Hickenlooper (D-Colo.) spoke about the need for bipartisan legislation on crypto, saying a bill may be introduced in the coming weeks.

Friday

- 18:00 UTC (2:00 p.m. ET) There will be an omnibus hearing in the FTX bankruptcy case.

Elsewhere:

- (The Wall Street Journal) The U.S. Department of Justice is looking into terraUSD’s meltdown from last year, the WSJ reported.

- (Sports Illustrated) I don’t follow baseball, nor does this story have anything to do with crypto. It’s just very funny.

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at nik@coindesk.com or find me on Twitter @nikhileshde.

You can also join the group conversation on Telegram.

See ya’ll next week!

Learn more about Consensus 2023, CoinDesk’s longest-running and most influential event that brings together all sides of crypto, blockchain and Web3. Head to consensus.coindesk.com to register and buy your pass now.

DISCLOSURE

Please note that our privacy policy, terms of use, cookies, and do not sell my personal information has been updated.

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.

:format(webp)/www.coindesk.com/resizer/BETd9o0r2OHtd2vT2ZqY9QPrJps=/arc-photo-coindesk/arc2-prod/public/ODFQHDRZFJG7XNVO7P6PUYMWS4.png)

Nikhilesh De is CoinDesk's managing editor for global policy and regulation. He owns marginal amounts of bitcoin and ether.

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/HHAZAAXSBJD3NLASNFQDKP3WOE.png)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/3XAH3BH7BZE5ZNY2XTZ5BLD7QI.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/MM3UAOZCG5AUZIPOQ65VFTGA4U.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/Z3I2HMMBABCOJMIVKQT34UWXHI.jpg)