:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/KOKIGZKYNJF7LNLA3RQ6WRWY6A.jpg)

Nikhilesh De is CoinDesk's managing editor for global policy and regulation. He owns marginal amounts of bitcoin and ether.

It seems the crypto industry still has some questions about Signature and Silvergate’s shutdowns. Plus, I’m in Washington, D.C., for a few days this week attending the DC Blockchain Summit on Tuesday and the CFTC Technology Advisory Committee meeting on Wednesday. Say hi if you’re there!

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

Banking confusion

The narrative

We’ve still got some unanswered questions about the Signature and Silvergate bank shutdowns. What kinds of issues forced those shutdowns? Did Silvergate voluntarily repay its FHLB loans? Just how much money did Signature lose in deposits?

Why it matters

I think it’s safe to assume people want certainty. Companies want to know they'll be able to tap banking services. For that to happen, banks need to be comfortable serving crypto companies. And for that to happen, they probably need to know what factors led to Signature becoming a failed bank – was it, as so much of the industry keeps saying, the mere fact it served crypto clients? Or was it because the bank itself had some deeper issues?

Breaking it down

Things are pretty weird.

On Sunday, the Federal Deposit Insurance Corporation announced that Flagstar Bank, a subsidiary of New York Community Bancorp, would acquire the assets of Signature Bank – except for about $4 billion in crypto-related deposits. The Federal Deposit Insurance Corporation will dispose of those on its own (and in the meantime, the FDIC continues to operate Signature’s Signet system).

The news came days after Reuters reported the FDIC was telling potential bidders they would not be able to bid on the crypto parts of Signature’s business, a claim the FDIC denied.

This came days after my colleague Helene Braun reported the Federal Home Loan Bank of San Francisco denied it forced Silvergate Bank to repay its loans, though FHLB declined to answer whether that meant it refused to roll its advance to Silvergate.

My colleague Jesse Hamilton also reported Monday that major banks aren’t rushing to fill the Signature/SIlvergate-shaped hole for crypto companies. A number of major banks have outright said they are not looking to provide services for the crypto industry, or at least not for companies that engage directly with tokens. Other banks are willing to work with companies that invest in companies that deal with crypto – they’re OK with crypto at a distance, basically.

Suffice to say, however, there seems to be more to the story behind Signature and Silvergate than we know at this moment. Both banks appeared to experience major outflows prior to their respective shutdowns. While we don’t have reliable figures for Silvergate at this time, we can compare Signature’s last reported figures with what the FDIC has shared.

On March 8, Signature reported it held over $89 billion in deposits, about $16.5 billion of which were tied to the crypto industry. As of March 19, the crypto deposit figure was down to $4 billion – suggesting that more than $12 billion in deposits from crypto companies left Signature in a very short period of time.

If other depositors followed suit, a good chunk of Signature’s deposits may have left after that March 8 press release. Barney Frank, the former congressman and current Signature Board member going around saying it was shuttered due to politics or crypto, said $10 billion left the bank on March 9.

We’re also still waiting on updated figures from between March 12, when the New York Department of Financial Services seized Signature, and March 19, when the FDIC approved Flagstar’s bid.

All this is to say we’re in a pretty weird spot in terms of guessing what the future may look like for crypto companies seeking banking services. It’s almost a throwback to years past, when crypto companies couldn’t secure reliable banking services on their own.

Stories you may have missed

- EU Parliament’s Smart Contract Plans Limit Standard-Setting Promise, EU Commissioner Says: The European Parliament passed a bill mandating a kill switch in smart contracts.

- Is This a Crypto Banking Bailout?: Was last week’s actions by federal bank regulators and the U.S. Treasury Department to backstop deposits at failed banks a bailout?

SCOTUS takes up crypto (sorta)

By Cheyenne Ligon

The U.S. Supreme Court will hear arguments in its first crypto-related case on Tuesday, when lawyers for San Francisco-based crypto exchange Coinbase will attempt to convince the nine Justices to pause a pair of class-action lawsuits against the crypto exchange.

Though the case the high court will hear Tuesday involves crypto, it is not itself a crypto case. Instead, this case is a fairly esoteric, procedural argument over whether a lawsuit can proceed in federal court while one party – in this case, Coinbase – is attempting to send the dispute to arbitration.

Coinbase is in the process of appealing an earlier decision by a federal court in California allowing the two lawsuits, Bielski v. Coinbase and Suski v. Coinbase, to continue, in contrast with Coinbase’s user agreement, which requires disputes to be sent to arbitration. Arbitration is an out-of-court method of dispute resolution in which the odds are often unfairly stacked against consumers.

This week

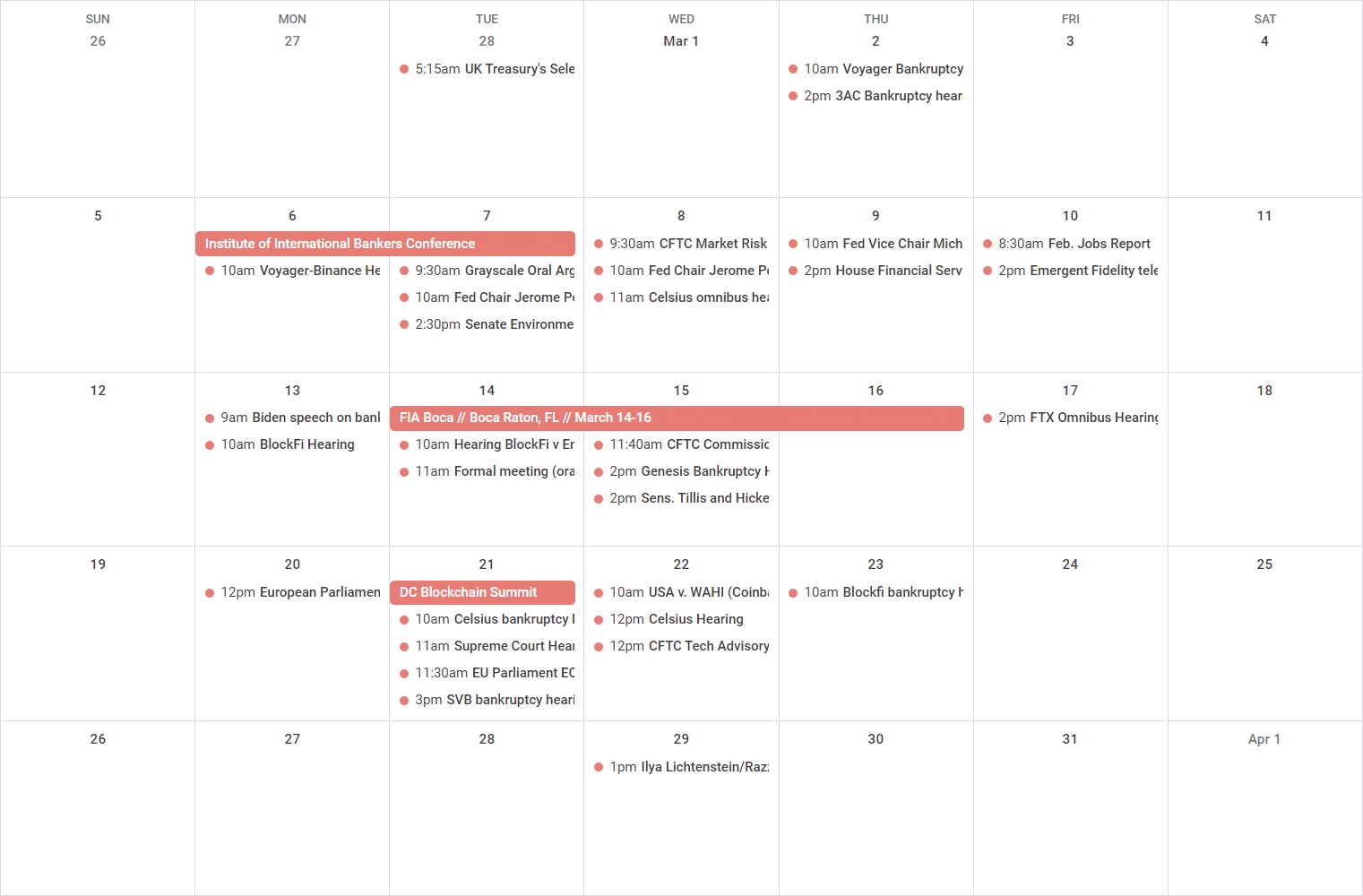

Monday

- 16:00 UTC (12:00 p.m. ET/5:00 p.m. CET) European Central Bank President Christine Lagarde spoke to the European Parliament, saying a bank run on a future digital euro wouldn’t be likely if there's a limit on the amount of digital euros any person can have at a given time.

Tuesday

- 13:00 UTC (9:00 a.m. ET) The DC Blockchain Summit is being held today. I plan to be around. Say hi!

- 14:00 UTC (10:00 a.m. ET) There's a Celsius Network bankruptcy hearing.

- 15:00 UTC (11:00 a.m. ET) The U.S. Supreme Court will hear its first crypto-related case. Court begins at 10:00 a.m. ET but there will be another hearing prior to Coinbase, and each case is expected to last about an hour.

- 15:30 UTC (11:30 a.m. ET / 16:30 CET) The European Parliament’s ECON committee will hold a hearing on financial stability in Europe in the wake of Silicon Valley Bank’s collapse.

- 19:00 UTC (3:00 p.m. ET) Silicon Valley Bank will have its first bankruptcy hearing.

Wednesday

- 14:00 UTC (10:00 a.m. ET) There will be a status update hearing in USA v. Wahi.

- 16:00 UTC (12:00 p.m. ET) There will be another Celsius hearing, focused on services agreements.

- 16:00 UTC (12:00 p.m. ET) The CFTC will hold its first Technology Advisory Committee meeting under new sponsor Commissioner Christy Goldsmith Romero. I plan to be here as well!

Thursday

- 14:00 UTC (10:00 a.m. ET) There will be an update hearing in BlockFi’s bankruptcy case.

Elsewhere:

- (Politico) Politico profiled Congressman Patrick McHenry (R-N.C.), the chair of the House Financial Services Committee.

- (Fortune) Fortune reports that crypto exchange Coinbase offered to backstop USDC after the stablecoin broke its dollar peg the other weekend on news that issuer Circle had $3.3 billion locked up at Silicon Valley Bank.

- (The Washington Post) The Post reports Tesla CEO Elon Musk wanted his electric cars to be cheaper so he forced the removal of a radar system. “The result, according to interviews with nearly a dozen former employees and test drivers, safety officials and other experts, was an uptick in crashes, near misses and other embarrassing mistakes by Tesla vehicles suddenly deprived of a critical sensor.”

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at nik@coindesk.com or find me on Twitter @nikhileshde.

You can also join the group conversation on Telegram.

See ya’ll next week!

Learn more about Consensus 2023, CoinDesk’s longest-running and most influential event that brings together all sides of crypto, blockchain and Web3. Head to consensus.coindesk.com to register and buy your pass now.

DISCLOSURE

Please note that our privacy policy, terms of use, cookies, and do not sell my personal information has been updated.

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.

:format(webp)/www.coindesk.com/resizer/BETd9o0r2OHtd2vT2ZqY9QPrJps=/arc-photo-coindesk/arc2-prod/public/ODFQHDRZFJG7XNVO7P6PUYMWS4.png)

Nikhilesh De is CoinDesk's managing editor for global policy and regulation. He owns marginal amounts of bitcoin and ether.

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/HHAZAAXSBJD3NLASNFQDKP3WOE.png)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/3XAH3BH7BZE5ZNY2XTZ5BLD7QI.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/MM3UAOZCG5AUZIPOQ65VFTGA4U.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/Z3I2HMMBABCOJMIVKQT34UWXHI.jpg)