:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/SXTC4TFQCNCXZKH7ODEOCYIRJI.jpg)

Nikhilesh De is CoinDesk's managing editor for global policy and regulation. He owns marginal amounts of bitcoin and ether.

Between Coinbase, Binance, Justin Sun, Do Kwon and Custodia, there has been just so much news over the last week. And that’s largely just the U.S. But Binance is the most interesting, not only for what happened (the Commodity Futures Trading Commission sued it), but also for what didn’t (the Department of Justice hasn’t filed anything). Plus, the CFTC’s Tech Advisory Committee met last Wednesday.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

Binance Gets Sued

The narrative

The U.S. Commodity Futures Trading Commission (CFTC) sued Binance, the exchange’s founder Changpeng Zhao (CZ) and a couple other entities on Monday on charges of failing to register as a “futures commission merchant” while offering unregistered crypto derivatives options to U.S. customers.

Why it matters

The allegations are pretty striking, with details suggesting the company went out of its way to try to bypass U.S. regulations. CFTC Chief Counsel Gretchen Lowe described Binance’s actions as “willful evasion of U.S. law.” These are allegations that have yet to be proven in a court of law. In a statement Monday night, Zhao said the allegations are “an incomplete recitation of facts.”

Breaking it down

The question remains: Is this actually a big deal for Binance? I’m going to speculate wildly, so consider this fair warning.

I think the answer is yes. Not for the CFTC charges themselves – the CFTC can impose monetary fines and bar Zhao from being an officer at a futures commission merchant in future but that assumes Zhao has any interest in being an officer to begin with.

The allegations in the CFTC’s complaint have strong implications for criminal and sanctions-related issues.

Some of the claims in the lawsuit, such as allegations that the exchange was aware that people from sanctioned entities such as Hamas, a Palestinian militant group, were trading on the platform but didn’t see it as a big deal, would probably trigger both Department of Justice and the Treasury Department’s Office of Foreign Asset Control laws.

“[Binance’s former Chief Compliance Officer Samuel] Lim explained to a colleague that terrorists usually send ‘small sums’ as ‘large sums constitute money laundering,” the filing said. “Lim’s colleague replied: ‘can barely buy an AK47 with 600 bucks.’ And with regard to certain Binance customers, including customers from Russia, Lim acknowledged in a February 2020 chat: ‘Like come on. They are here for crime.’ Binance’s [money laundering reporting officer] agreed that ‘we see the bad, but we close 2 eyes.’”

The CFTC complaint emphasized that Binance uses U.S. services to operate, pointing to Google Suite, Webex, WeWork and Amazon Web Services as examples.

“Among the services Binance purchases from Amazon Web Services that are provided to Binance in the United States is ‘AWS CloudFront,’ which according to Amazon Web Services is a ‘Global content delivery network,’” the filing said.

We’ve known for a while now that Binance used AWS servers in Japan after an outage affected the exchange a few years ago.

The final piece of this puzzle: We can look at how the Department of Justice has gone after companies and websites accused of distributing ransomware or offering “cyberattack-for-hire services” or even whatever the heck this was.

In those instances, the U.S. government was able to seize the domains and put up a large banner announcing that. The services themselves were inaccessible to their users.

All this is to say that if the U.S. really thought Binance was a criminal enterprise, it already has the tools it needs to shut down the exchange.

Now to be clear, I’m told there's nothing imminent coming from the Justice Department or Office of Foreign Asset Controls about Binance. But as we’ve seen with Terraform Labs founder Do Kwon and FTX founder Sam Bankman-Fried, sometimes the DOJ will have a sealed indictment that it won’t publish until the subject is arrested, and so we may now just be in a holding pattern.

Stories you may have missed

- Do Kwon Arrested in Montenegro: Interior Minister: Do Kwon, creator of the Terra network and UST stablecoin, was arrested in Montenegro last week after he tried to fly out of the country with a falsified passport, Interior Minister Filip Adzic said.

- Do Kwon Now Faces Criminal Fraud Charges From U.S. Prosecutors: After Kwon was arrested in Montenegro, the U.S. Department of Justice unveiled a litany of charges against him.

- Tron Founder Justin Sun Sued by SEC on Securities, Market Manipulation Charges: So true story: I picked someone up from JFK International Airport in New York over the weekend, and on my way out, I saw a large electronic billboard with a Tron ad that featured founder Justin Sun on it. Anyways, he’s facing civil charges from the U.S. Securities and Exchange Commission, alleging he engaged in market manipulation of unregistered securities (TRX and BTT), among other things.

- SEC Warns Coinbase It's Pursuing Enforcement Action Over Securities Violations: Coinbase received a Wells Notice from the SEC, alleging that certain listed tokens, its staking program and other products may all violate federal securities laws.

- Crypto’s Unfulfilled Dreams Get a Tailwind From U.S. Crackdown on Binance, Coinbase: CoinDesk’s Helene Braun took a look at what recent regulatory actions might mean for decentralized exchanges.

- EU Lawmakers to Vote on Limited Ban on Self-Hosted Crypto Payments: European Union lawmakers planned to vote on a possible ban on crypto transfers of more than 1,000 euros ($1,084) from self-hosted wallets, CoinDesk’s Jack Schickler reported. Transfers where the parties’ identities can be verified or between two private individuals would be allowed. Lawmakers voted in favor of the bill a day later.

- Federal Reserve Says Custodia’s Plans Would Endanger Itself and the Crypto Industry: This was an absolutely rough report from the Federal Reserve Board on why it rejected Custodia Bank’s application for Fed membership. Custodia published a response a few days later.

Regulatory clarity in action

Terranet Ventures' Carole House, CFTC Commissioner Christy Goldsmith Romero (Nikhilesh De/CoinDesk)

Last week, the CFTC’s Technology Advisory Committee met for the first time under Commissioner Christy Goldsmith Romero, Chairwoman Carole House and Vice Chairman Ari Redbord.

“We look forward to taking a deep dive on the rapidly growing decentralized-finance (DeFi) ecosystem,” Goldsmith Romero said during her opening remarks. “As regulators and Congress make policy decisions related to DeFi, it is important to have a common foundation and understanding how DeFi works and how decentralized exchanges (DEXs) or other DeFi protocols [work].”

This foundation could be as basic as understanding what the indicators of decentralization are, she added, touching on other issues like the role of artificial intelligence in financial markets, digital identity and possible illicit activities in the digital sector.

The meeting was divided into presentations by various members interspersed by free-flowing discussions about issues surrounding regulatory questions in crypto (and other technology topics like artificial intelligence).

Different perspectives were all given equal weight by the different members of the committee, Goldsmith Romero told CoinDesk after the meeting ended, pointing to one participant who asked questions about the value crypto products brought the financial sector in a room full of crypto executives and researchers.

“People were very willing to contribute,” she said.

House said much of the discussion circled around the concept of accountability, which is at the heart of many of the topics discussed, whether that is privacy or decentralized finance or other issues.

“There has to be accountability, both for the regulated activity … but also for the non-financial activity that occurs,” she said.

Goldsmith Romero expressed a similar view during her opening remarks, saying there is discussion about where accountability rests within a DeFi project, whether it’s the code underpinning a smart contract, the organization responsible for bringing the code into the world, an evolving governance structure or something in between.

The forum saw a nuanced discussion about how different parties could achieve confidence in the technology around digital assets and other issues while still ensuring compliance with the law, Goldsmith Romero said after the meeting ended. “I’m glad to have that in this forum.”

Wherefore art thou Signature

There was much ado made the other week about New York Community Bancorp’s (NYCB) Flagstar Bank acquiring Signature Bank’s non-crypto deposits last Monday, leaving about $4 billion worth of deposits in the lurch. Coming on the heels of a Reuters report that the Federal Deposit Insurance Corp. (FDIC) would force any potential buyer of Signature to give up the crypto business (a report the FDIC denied), there was a growing wave of opinion that this was further evidence that bank regulators were trying to actively boot crypto off the banking system. As always, though, it’s possible things are a bit less conspiratorial than the public narrative seems.

Joshua Ashley Klayman, head of blockchain and digital assets at law firm Linklaters, pointed to 2021 guidance from the Office of the Comptroller of the Currency (OCC), one of the federal bank regulators, that told banks that they need permission before they can get into crypto-related activities. The regulator has already barred one new conditional bank from engaging with crypto when it approved SoFi in 2022, she said.

“It shouldn’t be a surprise that, as any bidding bank presumably would need OCC approval, that, if they didn’t already have OCC approval to engage in digital asset activities, they weren’t reasonably going to be able to obtain it over a weekend, even if they wanted to start doing crypto,” Klayman said.

Klayman noted that “we don’t know if Flagstar even wanted to have a crypto business, or if it even had the capability to support one. But it almost certainly didn’t have the time to obtain regulatory approval to start one by Monday.”

Only 136 FDIC-insured banks in the U.S. even offer any kind of crypto activities or plan to, according to an FDIC Inspector General report from February. That’s out of 4,706 total FDIC-insured banks (as of the end of 2022).

The FDIC is now giving the remaining Signature Bridge Bank depositors until April 5 to withdraw their funds, or the regulator will send a check to the listed address. It’s also still trying to sell the Signet platform, a payments platform that was popular with Signature’s crypto customers.

This past weekend, the FDIC said that First Citizens Bank will acquire the deposits from Silicon Valley Bank. One detail that struck me: When the FDIC announced Flagstar’s takeover of Signature deposits, it explicitly said that Signature Bridge Bank depositors “other than cash depositors related to the digital-asset banking businesses, will automatically become depositors of” Flagstar.

No such language existed in the announcement of First Citizens’ takeover of SVB deposits. I reached out to the FDIC and First Citizens to confirm just what this meant. The FDIC referred me to First Citizens, which hasn’t responded.

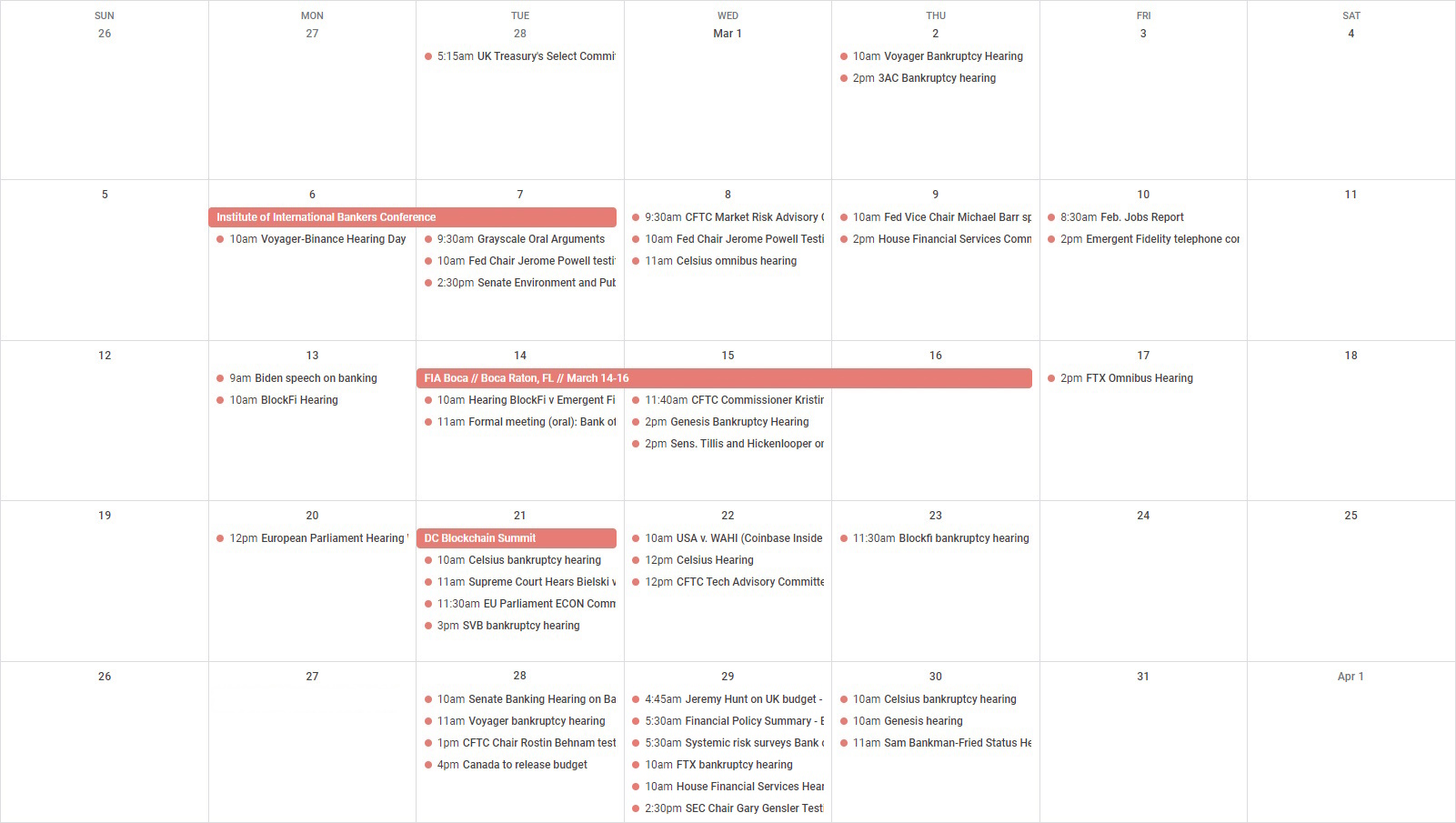

This week

Tuesday

- 14:00 UTC (10:00 a.m. ET) The Senate Banking Committee held a hearing on the recent bank failures.

- 15:00 UTC (11:00 a.m. ET) There was a status update hearing in the ongoing Voyager Digital bankruptcy case.

- 17:00 UTC (1:00 p.m. ET) CFTC Chair Rostin Behnam testified before a subcommittee on the House Appropriations Committee to discuss the agency’s budget for the upcoming fiscal year.

- 20:00 UTC (4:00 p.m. ET) Canada published its budget, including a crypto provision.

Wednesday

- 8:45 UTC (9:45 a.m. BST) U.K. Chancellor of the Exchequer Jeremy Hunt will speak on the U.K.’s budget in front of the nation’s Treasury committee.

- 14:00 UTC (10:00 a.m. ET) There will be an FTX bankruptcy hearing.

- 14:00 UTC (10:00 a.m. ET) The House Financial Services Committee will hold a hearing on the recent bank failures.

- 18:30 UTC (2:30 p.m. ET) SEC Chair Gary Gensler will testify before a subcommittee on the House Appropriations Committee to discuss the agency’s budget for the upcoming fiscal year.

Thursday

- 14:00 UTC (10:00 a.m. ET) There will be a Celsius bankruptcy hearing.

- 14:00 UTC (10:00 a.m. ET) There will also be a Genesis bankruptcy hearing.

- 15:00 UTC (11:00 a.m. ET) There will be a hearing on Sam Bankman-Fried’s ongoing criminal case.

Elsewhere:

- (The Wall Street Journal) A number of banks are getting more involved in crypto in the wake of Silvergate and Signature collapsing, the Journal reports.

- (CNBC) CNBC has a massive report about how Binance encouraged users to flout know-your-customer rules to access the exchange.

- (DL News) Some color on Do Kwon’s arrest: “The man once hailed as the ‘crypto king’ was traveling on a forged Costa Rican passport.”

- (Blockworks) “Florida Bill Banning CBDCs Might Accidentally Ban Bitcoin Too,” reads this headline.

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at nik@coindesk.com or find me on Twitter @nikhileshde.

You can also join the group conversation on Telegram.

See ya’ll next week!

Learn more about Consensus 2023, CoinDesk’s longest-running and most influential event that brings together all sides of crypto, blockchain and Web3. Head to consensus.coindesk.com to register and buy your pass now.

DISCLOSURE

Please note that our privacy policy, terms of use, cookies, and do not sell my personal information has been updated.

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.

:format(webp)/www.coindesk.com/resizer/BETd9o0r2OHtd2vT2ZqY9QPrJps=/arc-photo-coindesk/arc2-prod/public/ODFQHDRZFJG7XNVO7P6PUYMWS4.png)

Nikhilesh De is CoinDesk's managing editor for global policy and regulation. He owns marginal amounts of bitcoin and ether.

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/HHAZAAXSBJD3NLASNFQDKP3WOE.png)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/3XAH3BH7BZE5ZNY2XTZ5BLD7QI.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/MM3UAOZCG5AUZIPOQ65VFTGA4U.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/Z3I2HMMBABCOJMIVKQT34UWXHI.jpg)